The Age 55 Strategy: Why I Chose the $279,000 ERS Over a Cash Payout

“Most people celebrate their 55th birthday with a party. I celebrated mine by moving my money into a higher-paying bucket. Here is the story of my $279,000 milestone.”

In Singapore, turning 55 is often met with a mix of excitement and anxiety. You hear the rumors at the coffee shop: “The government is going to lock your money,” or “You’ll never see your OA again.” As an ordinary worker who spent 32 years navigating this system, I can tell you those fears are usually based on a lack of math. When I reached 55, I didn’t see a “lock”—I saw an opportunity to give myself a pay raise.

1. Understanding the Milestones: BRS vs. FRS vs. ERS

When my milestone arrived, the CPF board laid out three paths. It is important for every worker to understand these numbers, because the choice you make at 55 determines your “Ghost Salary” at 65.

- Basic Retirement Sum (BRS) – For those with property pledge.

- Full Retirement Sum (FRS) – The standard milestone.

- Enhanced Retirement Sum (ERS) – The maximum “Safe and Save” target.

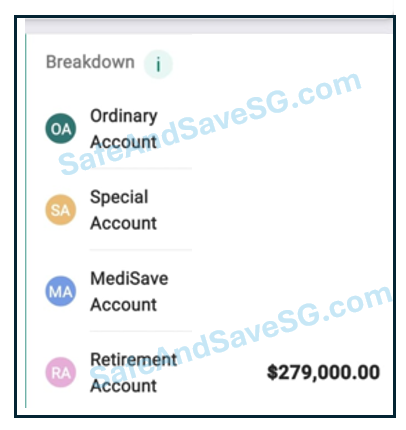

While many of my peers were satisfied with hitting the FRS ($186,000 in 2021) and withdrawing the rest for lifestyle spending, I decided to go for the Enhanced Retirement Sum of $279,000. I didn’t want the cash in my pocket to spend on things that lose value; I wanted the guaranteed interest for a future that lasts.

2. The Engineering Logic: The 1.5% “Arbitrage”

Why did I choose to move my Ordinary Account (OA) money into the Retirement Account (RA)? It wasn’t about being “rich.” It was about simple efficiency. Look at the interest rates:

| Account Type | Interest Rate |

|---|---|

| Ordinary Account (OA) | 2.5% per annum |

| Retirement Account (RA) | 4.0% per annum (Minimum) |

By moving $50,000 from my OA to my RA, I instantly gave that money a 1.5% pay raise. Over 10 years, that extra 1.5% compounding on $279,000 creates a massive difference in the final payout. This is what I call “Safe and Save”—no stocks, no crypto, no risk. Just moving money between buckets to get the best yield.

Check the latest Retirement Sum milestones:

Official CPF: Retirement Sum Guide ›3. Dealing with the “What Ifs”

People often ask: “Peter, what if you need that money for an emergency?”

This is the secret: After you hit your FRS/ERS at age 55, any amount left in your OA and SA is actually withdrawable at any time. It essentially becomes a high-interest savings account. By topping up my RA to the ERS first, I secured my lifelong “Ghost Salary,” while my remaining OA became my flexible safety net for medical bills or home repairs.

4. The 10-Year Compounding Runway

Between the age of 55 and 65, your RA sits there and works for you. Every year, the 4% interest is added to the principal. In my case, starting with the $279,000 ERS and adding my tactical transfers meant that my RA grew significantly. This is how I reached the $440,800 level (the 2026 ERS) that sustains my monthly payout today.

Conclusion: The Reward for Patience

Reaching the $279,000 ERS wasn’t luck. It was the result of 32 years of showing up and being disciplined. While others were withdrawing their funds at 55 to buy luxury items, I was reinvesting in my own freedom. Today, my “Ghost Salary” is the reward. If you are approaching 55, don’t just settle for the minimum—look at the ERS. Your future self will thank you.

Next Step in the Blueprint:

Why I Chose the $2,830 Life-Long Salary ›